Authors: David Neveselý, Vladek Krámek, Jiří Nečas

Inheritance tax was abolished in the Czech Republic at the end of 2013. The reason for this step was the very low income for the state budget and uneconomical collection. However, in the current atmosphere of the upcoming elections and unprecedented budget deficits caused by the ongoing pandemic, the topic of new taxes is increasingly being raised in public debate. Inheritance tax is also being raised as a topic for such debate. The Organisation for Economic Co-operation and Development (OECD), of which the Czech Republic is a member, has now also called for its introduction and increased importance for state budgets.

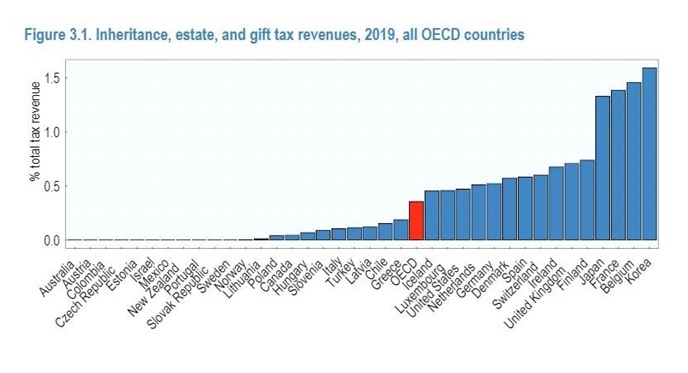

According to a newly released OECD report[1] the member states’ approaches to inheritance tax vary widely. While on the one hand there are countries such as the Czech Republic, where inheritance taxes do not exist, there are also countries such as South Korea, Belgium or France, which in certain cases burden the estate with up to an 80% rate.

Despite these international differences, the OECD believes that inheritance tax has great potential in the current situation in all countries. Not only can it help to fill leaky state budgets, but it can allegedly be used to solve the problem of the ever-widening gap between the richer and poorer sections of the population. Moreover, the organisation argues that collecting inheritance tax is not administratively and financially demanding and it is relatively easy for the authorities to detect attempts at tax evasion.

Thus, especially in countries with lower taxation of capital income - which includes the Czech Republic - the OECD has recommended greater use of inheritance taxes. According to the presented recommendations, they should introduce a tax progression that disadvantages those who inherit larger amounts of property. On the other hand, states should not introduce greater differences in the taxation of heirs according to their relationship to the testator, so as to avoid the accumulation of wealth in a narrow range of persons. Similarly, alongside inheritance taxes, they should introduce gift taxes.

There are no specific legislative proposals for the reintroduction of inheritance tax in the Czech Republic at the moment. However, the very possibility of introducing inheritance tax may pose a major problem for family business owners, for whom planning the transfer of property is usually a long-term matter.

No one can predict exactly what tax and other rules will apply at the time of their death and how their descendants will be affected. In other words, an owner who drew up a will today in respect to particular property does not know whether their heirs will actually receive the entire property or whether they will not overburden them too much with the inheritance and the associated tax. As foreign experience has shown, the tax liability can be so high that descendants are forced to sell the family business or core family assets (such as houses), often quickly and not infrequently below market value.

In addition, inheritance tax is just one of the many complications associated with inheritance. Even at the outset, inheritance proceedings can be the cause of protracted family disputes. Even if the family passes this test and can still manage the family business together, the problems do not end there. Even a well-drafted will cannot prevent, for example, the gradual fragmentation of property over a longer period or the transfer of property outside the founder’s family.

Last but not least, inheritance law does not, of course, address the potential threat to the family business before the death of its owner - for example, as a result of a major health disability, divorce or an attack by creditors. This threat also applies to any family member who inherits the family business in the future.

So, what can a family business owner do if they wish to mitigate these risks not only during their lifetime, but also after transferring their business to the next generation? In practice, the family foundation historically proven in Europe and the trust inspired from the Anglo-Saxon countries are increasingly proving useful.

Both of these legal institutes make it possible to hold the family property safely and as a single whole for a long time. The management of the family business or key assets is always carried out according to the wishes of the founder, who also determines the rules on how the income from the property is to be distributed among the family. The timely and in particular, high-quality establishment of a family foundation or trust will prevent all kinds of threats and suspicions of circumventing the tax rules while they are not yet set.

Our law firm is ready to discuss all the risks and options with you and prepare a tailor-made solution to your individual needs. We have the largest team of specialists in the Czech Republic with extensive experience in family foundations, trusts and intergenerational wealth transfer. We have assisted in the establishment of several hundred family foundations, trusts, other instruments of the holding and protection of private assets, through which assets in the high tens of billions of crowns are protected.

[1] OECD (2021), Inheritance Taxation in OECD Countries, OECD Tax Policy Studies, OECD Publishing, Paris, https://doi.org/10.1787/e2879a7d-en.